Can You Get a Loan on a Salvage Title in California?

Yes. Many rebuilt vehicles qualify for a title loan in California.

Most lenders require the car to have a revived salvage title, which means it has been repaired, passed a state inspection, and is legal to drive. The car also needs to be registered, insured, and in working condition.

Loan amounts are usually lower than for a clean-title car, but a salvage history alone does not automatically disqualify you.

How Much Can You Borrow?

Most title lenders lend about 25% to 50% of your car’s appraised value. With a salvage car, the difference comes down to the value itself.

A salvage or rebuilt history can cut a car’s market value by up to 40%, based on a long-standing Kelley Blue Book rule of thumb that deducts 20% to 40% from Blue Book value.

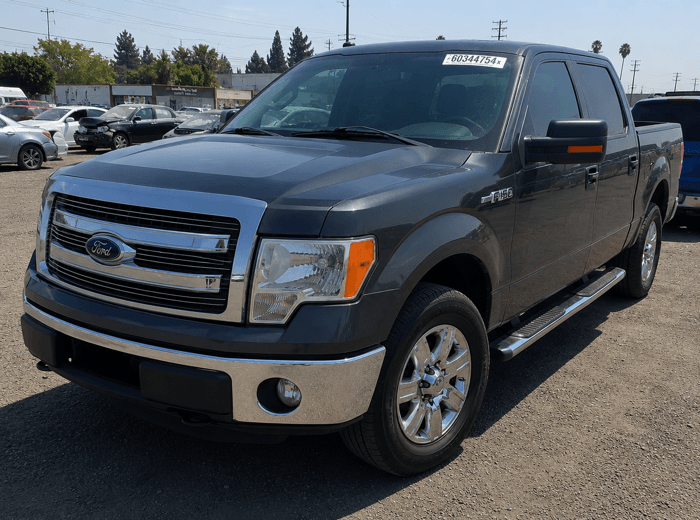

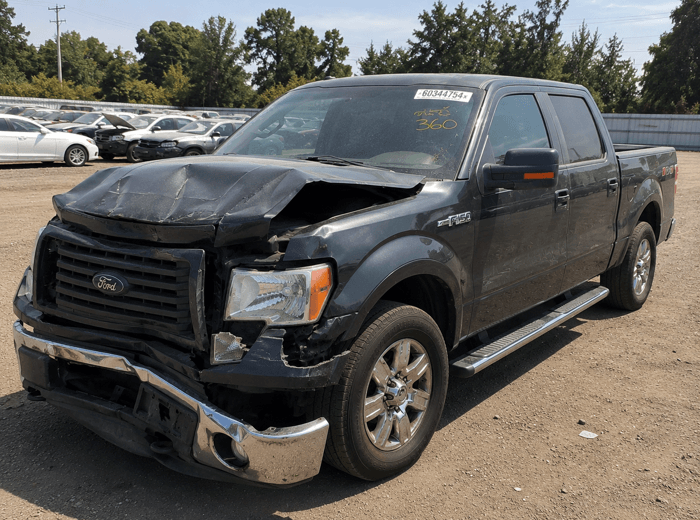

Here is how that looks in real numbers. The Ford F-150 was the vehicle we funded most often in 2025, so take a used F-150 worth about $12,500 with a clean title. A salvage history could bring that down to around $8,000.

At 25% to 50% of that $8,000, the most you could borrow is around $4,000. Most lenders also set a minimum loan near $2,510, so the realistic range on this truck is about $2,510 to $4,000.

On a higher-value vehicle, salvage title loans can reach into the tens of thousands of dollars.

Images are for illustration only.

How Fast Can You Get the Money?

Once your paperwork and inspection are done, funding moves quickly. At 5 Star, applications approved by about 2 p.m. can often be funded the same business day, and most others fund within one business day.

Key Takeaways

- A salvage title is a California DMV record showing the car was once declared a total loss.

- You can usually borrow only after the car has been repaired and re-titled as a rebuilt or revived salvage vehicle that passed California’s required safety inspection.

- We weigh your car’s value, its condition, and your income more than your credit score.

- A salvage history can cut a car’s value by 20% to 40%, so the loan is smaller than it would be on a clean-title car.

- Title loans come with high interest, so they are best saved for a real emergency, not everyday spending.

- Your car is the collateral. If you fall behind on payments, you could lose it.

What I Look At When I Evaluate a Salvage Car for a Title Loan

Bryan Solis

Head of Underwriting

Get the car repaired and keep your paperwork organized, and a salvage history alone usually will not prevent you from getting a title loan.

After more than 10 years in title loan underwriting, I’ve seen that two salvage vehicles with similar histories can receive very different loan offers.

The first thing I review is why the vehicle was totaled. Flood and fire damage typically carry more risk because hidden problems can appear later. Repaired collision damage is usually easier to evaluate.

Next, I look for proof of repairs. Repair invoices, parts receipts, and inspection records help verify the vehicle’s condition. The more documentation you have, the easier it is to support a higher valuation.

Finally, I check the basics. The vehicle must run safely, be registered in your name, and carry insurance. If the vehicle still has an unrepaired salvage title, it generally will not qualify.

The most common reasons for a decline are not the salvage history itself. More often, the vehicle’s value is too low, or the repairs cannot be verified. When those issues are addressed, many rebuilt vehicles can qualify.

What Is a Salvage Title in California?

In California, a salvage title is really a salvage certificate issued by the California DMV. A car gets one after it is declared a total loss.

This usually happens when an insurance company decides the car is too damaged or too costly to repair and pays out the claim. Once that record exists, anyone who checks the title can see the car was badly damaged at some point.

California sorts totaled cars into two groups:

- Repairable. The DMV issues a salvage certificate. After the car is rebuilt and passes California’s required vehicle safety systems inspection through the Bureau of Automotive Repair, plus a CHP vehicle verification, it can be re-titled as a revived salvage, often called a rebuilt title, and driven legally again.

- Non-repairable. If the car is too far gone, the DMV issues a non-repairable vehicle certificate. That car can never be registered for the road again, so it cannot be used as collateral for a title loan.

This is why almost every salvage title loan in California is really a loan on a rebuilt or revived salvage car. The car has to be road legal first.

How Can I Tell If My Car Has a Salvage or Rebuilt Title?

Not sure where your car stands? Here are three easy ways to check:

- Read your California title. Look near the top of your Certificate of Title for a brand like “Salvage” or “Revived Salvage.” A revived salvage brand means the car was once a total loss but has since been repaired and passed inspection.

- Run a VIN history report. Enter your 17-digit VIN at CARFAX or AutoCheck to see salvage records, major accidents, and past title changes. Want a free option first? The NICB VINCheck tool is no cost and flags salvage and total-loss records.

- Ask the California DMV. Request your vehicle’s record from the California DMV to confirm its current title status and registration history.

How Salvage Title Loans Work

A salvage title loan is a secured loan. You use the equity in your salvage or rebuilt car as collateral to get cash.

Unlike a bank loan, your credit history is not the main thing lenders look at. The value of your car and your income matter the most.

After you sign the loan agreement, you get your funds and keep driving your car. The lender places a lien on your title, which is its legal claim to the vehicle until the loan is paid off.

If you fall behind, the lender can repossess the car, though most would rather work with you than take that step.

What You Need to Apply in California

A salvage or rebuilt car gets a closer look than a clean-title car, so it helps to have your paperwork ready first. In California you will generally need:

- Vehicle title. The rebuilt or revived salvage title, in your name.

- California registration. Proof the car is currently registered with the California DMV.

- Photo ID. A valid California driver’s license or state ID.

- Proof of income. Recent pay stubs, bank statements, or other proof you can make the payments.

- Proof of residence. A recent utility bill or lease that matches your ID.

- Proof of insurance. Current coverage on the vehicle.

- Vehicle inspection. An inspection and appraisal to confirm the car’s condition and current value.

Having these ready can make the whole process faster.

What It Costs and What to Think About Before You Borrow

A title loan can solve a short-term cash problem, but it is important to understand the trade-offs first.

The Cost Is High, So Use It Only for an Emergency

Title loans charge far more interest than a bank or credit card, so they are built for a true emergency, not regular spending.

Under the California Financing Law, the rate on a title loan from $2,500 to $10,000 is capped at 36% per year plus the federal funds rate. That cap is a middle band, so loans under $2,500 or over $10,000 are not covered and can cost more.

Most title lenders set a minimum loan around $2,510, so if your car appraises too low to reach that, you may not qualify.

Your Car Is the Collateral

Because the loan is tied to your car, falling behind can lead to repossession. In California, a lender can repossess the car after default, but you must be notified before it is sold, and you generally have a chance to catch up and get the car back.

It Is Built for the Short Term

A title loan is meant to cover a temporary gap, not an ongoing shortfall. If the payments would strain your budget month after month, compare other options first, such as a personal loan, a credit union loan, or a local assistance program.

The California Department of Financial Protection and Innovation and the Federal Trade Commission both publish free guidance on car title loans.

Still not sure a title loan is the right move? See whether a title loan is right for you before you apply.

Frequently Asked Questions

Can You Finance a Salvage Title Vehicle in California?

Yes, but options are limited compared with a clean-title car. Most lenders will only lend on a salvage car after it has been repaired, inspected, and re-titled as a rebuilt or revived salvage vehicle. Loan amounts are usually lower because the car is worth less.

Can a Salvage Title Be Cleared in California?

A salvage title is never erased, but it can change. Once a repairable salvage car passes a brake and light inspection and a CHP vehicle verification, the California DMV can issue a revived salvage title, also called a rebuilt title, so the car can be registered and driven again. The history still shows on the record.

Does a Salvage Title Affect Getting a Loan?

Yes. A salvage history lowers the car’s value and makes it harder for a lender to resell if the loan is not repaid. That usually means a smaller loan, a closer inspection, and sometimes higher rates or fees than a clean-title car.

Can You Insure a Salvage Title Car in California?

Often yes, but coverage can be limited. Many insurers will offer liability coverage on a rebuilt car, while full coverage can be harder to get or cost more. Lenders usually require current insurance before they fund the loan.

How Much Can I Borrow With a Salvage Title Loan in California?

It depends on your car’s appraised value. Most title lenders lend about 25% to 50% of that value, and salvage cars appraise lower than clean-title cars, so your maximum is reduced. Many lenders set a minimum loan around $2,510, so if your car appraises for less than that, you may not qualify.